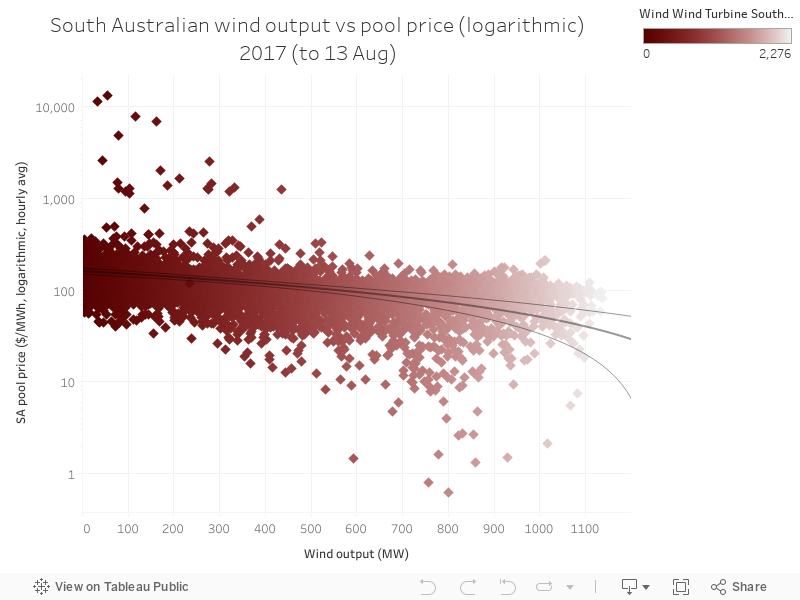

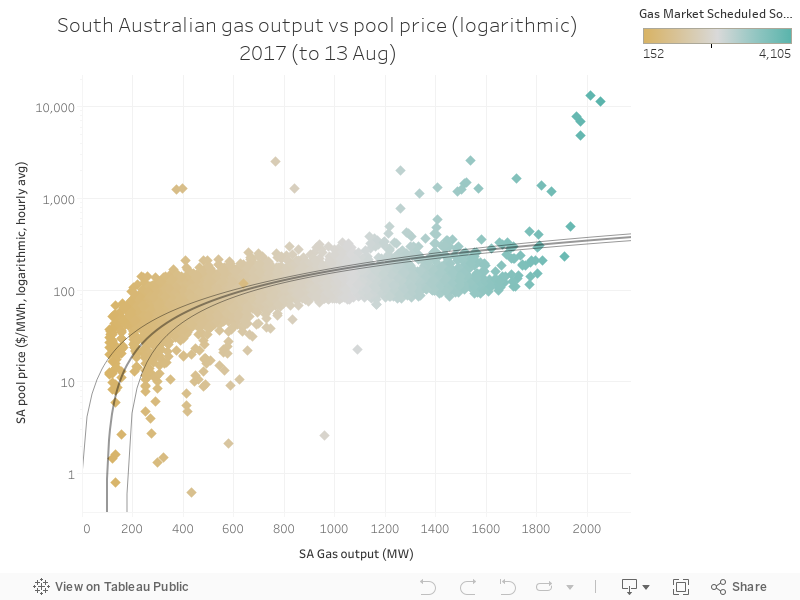

This week, a series on South Australia - all using data from Global Roam's excellent NEM Review software, which you can purchase

here.

Today's chart is similar to yesterday's - it shows the relationship between wind power output and wholesale price in South Australia. Unlike yesterday's chart on gas, wind has the opposite effect - as you get more wind power output in each interval, the price ends up lower. This is because wind introduces more competition, has no fuel costs, and also receives revenue from the Renewable Energy Target (RET) scheme - all of these factors mean wind's increasing output results in lower wholesale price in SA.

This is good, but obviously the impact varies with wind power output in the state. Once wind starts being paired with firming output - including storage technologies - we're going to see some very big changes in this dynamic. Obviously, wind will be slightly more expensive, but at the same time, it'll be dispatchable - and perhaps, as battery costs fall, it might end up even cheaper. Good times.